Experian vs CIBIL: Why Your Scores Differ & Which Matters for Loans

You just checked your credit score on two different websites.

CIBIL says: 750 Experian says: 720

Same person. Same day. Different numbers.

You're confused. Which one is right? Which one matters for your loan?

Here's the answer that surprises most people: Both are right. And both matter.

The Quick Answer

CIBIL: Most Indian banks use it. Most important.

Experian: Growing with fintech. Increasingly important.

Strategy: Improve both. Focus on CIBIL first.

Now, let me explain why they're different and why it matters.

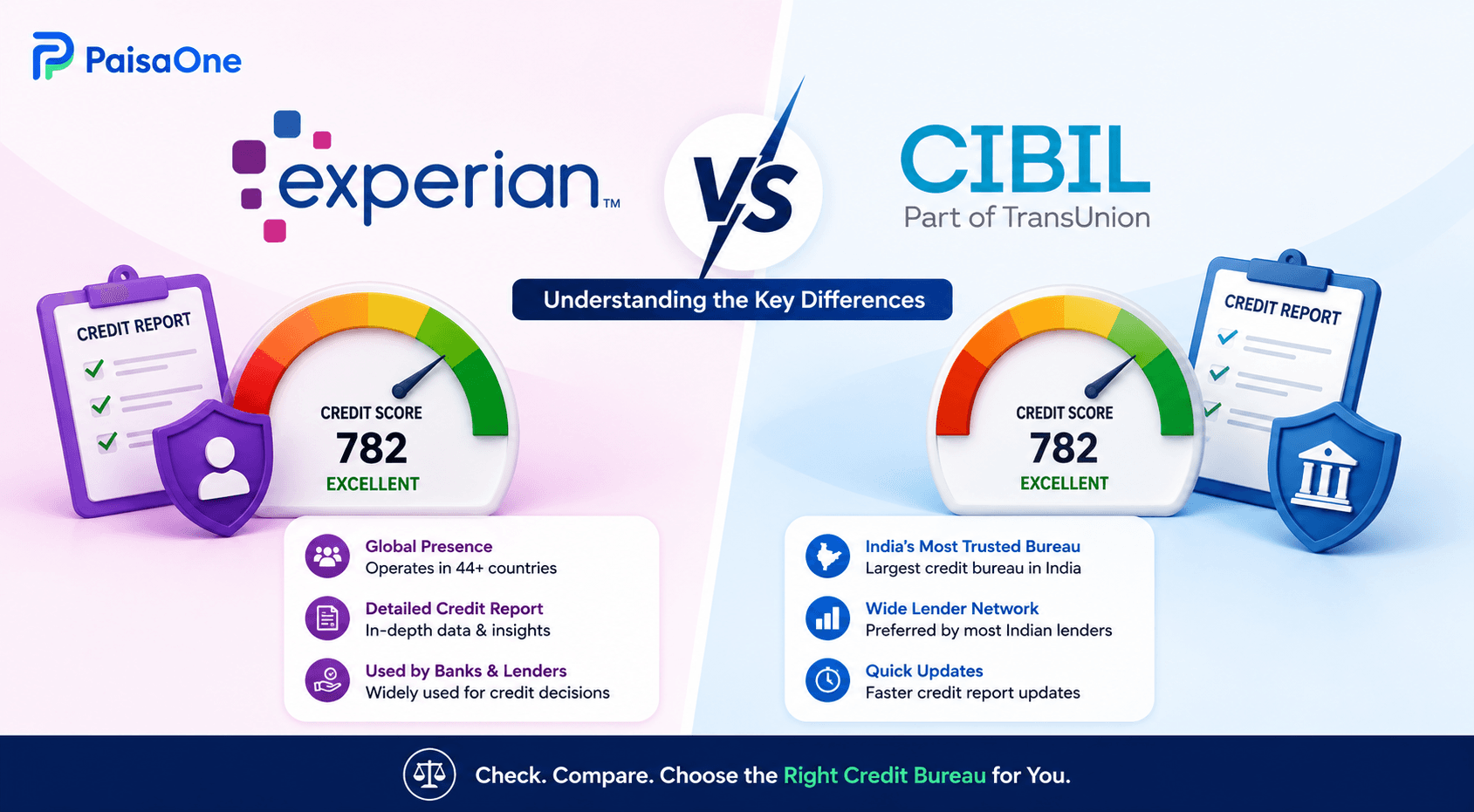

CIBIL vs Experian: Quick Comparison

What is CIBIL? (India's Original)

CIBIL = Credit Information Bureau India Limited (now TransUnion CIBIL)

Established in 2000, CIBIL was India's first credit bureau. It's the most recognized, most used, and most influential score in Indian lending.

When you apply for a home loan at SBI, HDFC, or ICICI Bank, they check your CIBIL score first.

CIBIL collects data from its member institutions (banks, NBFCs, credit card companies) and calculates a score from 300-900.

What this means: 90% of your loan applications will be evaluated primarily on your CIBIL score.

Read More: What Is CIBIL Score? How It Affects Your Loan Approval

What is Experian? (The Global Player)

Experian = Experian Credit Information Company of India Pvt Ltd

Global company with 125+ years of experience worldwide. Entered India in 2010.

Experian uses a FICO-based model (same model used in the US) and collects data from broader sources: banks, credit card companies, rental payment history, utility bills, and public records.

Experian scores range from 300-850 (mostly), though some platforms show 300-900.

What this means: Growing importance with fintech platforms, digital lenders, and NBFCs. Increasingly crucial as Indian lending becomes more tech-driven.

Why Your CIBIL and Experian Scores Are Different

Your CIBIL score is 750 but Experian is 720. You're worried. Don't be. Here's why they differ:

Reason 1: Different Scoring Algorithms

CIBIL uses a proprietary model designed specifically for Indian financial behavior.

Experian uses a FICO model, developed in the US, adapted for India but with global DNA.

These algorithms weight factors differently:

CIBIL: Emphasizes credit utilization ratio (30% weight) Experian: Emphasizes payment consistency/history (35% weight)

Example: You maintain 20% credit utilization (excellent) but had one late payment 6 months ago (recovered).

CIBIL scores you higher (utilization excellent)

Experian scores you lower (recent late payment still impacts)

Reason 2: Different Data Sources

CIBIL: Collects only from member institutions (banks, NBFCs) Experian: Collects from wider sources (rental payments, utility bills, public records)

If you pay rent on time (not through the formal system), Experian may see this. CIBIL won't. This can improve your Experian score.

Reason 3: Different Update Cycles

CIBIL and Experian receive lender updates on different schedules.

Your bank may report to CIBIL on the 5th, but to Experian on the 15th. So:

CIBIL reflects your latest payment status earlier

Experian lags by 10+ days

If you paid a late EMI on the 3rd, CIBIL updates quickly. Experian still shows the late payment for another week.

Reason 4: Different Score Ranges

This is important:

CIBIL: 300-900 maximum

Experian: 300-850 maximum (usually)

A CIBIL score of 870 is excellent. But Experian's max is 850, so direct comparison fails.

Which Score Matters More for Your Loan?

Short answer: CIBIL for traditional loans, Experian for digital loans. Best practice: Improve both.

For Traditional Banks (SBI, HDFC, ICICI, Axis)

CIBIL is primary. They've been using CIBIL for 20+ years. Their lending models are built around CIBIL thresholds.

Home loan approval: Depends primarily on CIBIL score.

Car loan approval: Depends primarily on CIBIL score.

Personal loan approval: Depends primarily on CIBIL score.

Strategy: If applying to a traditional bank, prioritize CIBIL score above 700.

For Government Banks (SBI, Canara, PNB)

CIBIL is a strong preference. Government banks have even longer relationships with CIBIL.

Strategy: Make CIBIL score 700+ your target.

For NBFCs (Bajaj, L&T, Muthoot)

Both CIBIL and Experian. Many NBFCs check both to assess risk.

Strategy: Maintain both above 650+.

For Fintech/Digital Lenders (RazorpayX, CASHe, ZestMoney)

Experian is growing in preference. Newer lenders built systems on Experian and other bureaus.

Strategy: Experian score matters increasingly. Don't ignore it.

The Four Credit Bureaus in India

Most people know only CIBIL and Experian. But India has four:

1. TransUnion CIBIL (300-900) - Most used, established 2000 2. Experian (300-850) - Growing, established 2010 3. Equifax (300-900) - Emerging, licensed but less used 4. CRIF High Mark (300-900) - Newer, least used

For practical purposes: Focus on CIBIL (most lenders use it) and Experian (growing importance). Equifax and CRIF matter for specific lenders only.

Read More: How to Improve Your CIBIL Score

Real Scenario: Your Two Scores Explained

Scenario 1: CIBIL 750, Experian 720 (70-point gap)

Why? You probably have low credit utilization (benefits CIBIL) but moderate payment history (benefits Experian). Or you may have slight inconsistency in payments that CIBIL weights less but Experian penalizes more.

Action: Both are good scores. 750 on CIBIL is strong for traditional banks. 720 on Experian is acceptable for most lenders. You'll likely get approved everywhere but at possibly different rates.

Scenario 2: CIBIL 680, Experian 710 (30-point gap)

Why? You have excellent payment history (benefits Experian) but higher utilization (hurts CIBIL). Or you recently paid off a loan (benefits Experian quickly, CIBIL slower).

Action: CIBIL 680 is borderline for banks. Apply to NBFCs for better odds. Experian 710 is decent. Focus on improving CIBIL utilization to 30% to boost it.

Scenario 3: Both above 750

Action: Excellent. You can get approved by virtually any lender at competitive rates.

How to Improve Both Scores Simultaneously

Don't improve one and ignore the other. Universal behaviors improve both:

Action 1: Pay Everything On Time (impacts all bureaus equally)

Every on-time payment adds points to both

One late payment hurts both

Action 2: Keep Utilization Below 30% (CIBIL emphasis, but helps Experian)

Reduces ₹80,000 balance to ₹30,000 on ₹100,000 limit

Immediate impact on both

Action 3: Don't Close Old Credit Cards (impacts all bureaus)

Closing reduces credit age and mix

Hurts both scores

Action 4: Avoid Multiple Loan Applications (impacts all bureaus)

Each application = hard inquiry

Temporarily hurts both

Timeline: 30-60 days for quick improvements (utilization). 3-6 months for significant improvements (consistent payments).

How to Check Your Scores

Free annually:

CIBIL: cibil.com (free once/year)

Experian: experian.in (free once/year)

Paid access (if can't wait):

CIBIL: ₹550

Experian: ₹399

On PaisaOne: Check your scores instantly and see which lenders accept your profile.

Next Steps: From Understanding to Approval

Step 1: Check both scores (free on CIBIL.com and Experian.in)

Step 2: Understand your position

700+ on CIBIL? You're in good shape for banks.

650+ on Experian? You're solid for NBFCs/fintech.

Below 650? Work on improving first.

Step 3: Apply strategically

Going to a traditional bank? Ensure CIBIL 700+.

Going to fintech? Ensure Experian 650+.

Uncertain? Check both and apply where you're strongest.

Step 4: Compare offers on PaisaOne See which lenders will approve your profile, at what rates, based on both bureaus.

FAQ

Q: Should I worry if my scores differ by 50 points?

No. 50-point differences are normal. Both models are valid. What matters is whether both are above your target (700+ for banks, 650+ for NBFCs).

Q: Which score should I share with lenders?

Share both. Let them know your CIBIL and Experian scores. Transparency helps. Some lenders specifically ask for one or the other.

Q: Can I improve one without improving the other?

Partially. Paying rent on time improves Experian more than CIBIL. But consistent behavior improves both. Don't strategize "ignore one bureau"—improve all.

Q: Is one bureau more accurate than the other?

Both are accurate to their own methodologies. Neither is wrong. They're just different perspectives on your creditworthiness.

Q: Do I need to fix errors on both bureaus separately?

Yes. If you find an error on CIBIL, dispute it with CIBIL. If on Experian, dispute separately. Each bureau maintains independent records.

Q: Which score improves faster?

Experian can show improvements faster (weekly updates vs CIBIL's monthly updates). But CIBIL impacts more loans, so improvements there matter more.

Bottom Line

CIBIL and Experian aren't enemies. They're different perspectives on your credit health.

CIBIL: India's established standard (90% of banks use it)

Experian: Growing digital-lender preference

Smart strategy:

Focus on CIBIL first (most lenders use it)

Don't ignore Experian (increasingly important)

Improve behavior that helps both (on-time payments, low utilization)

Monitor both scores

Apply strategically based on both

Your score of 750 on CIBIL and 720 on Experian isn't confusing. It's normal. It's actually useful—gives you a fuller picture of your creditworthiness.

Check both on PaisaOne. Compare lenders. Apply confidently.

Divya

Divya Kumari is an SEO & Content Strategist with experience in organic traffic growth, topical authority building, and content-led SEO strategies. She specializes in creating user-focused content for finance and SaaS websites, helping brands improve visibility through structured content planning, internal linking, and search optimization techniques.